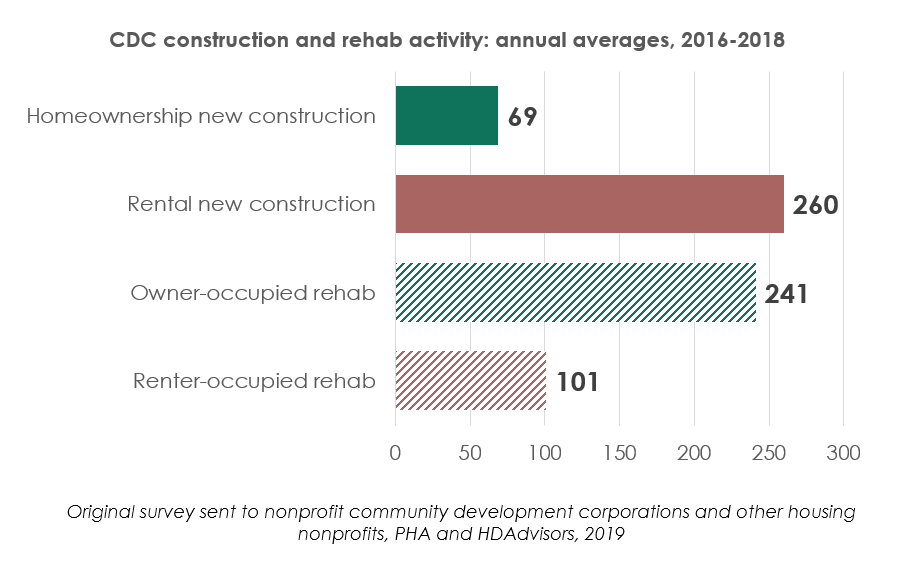

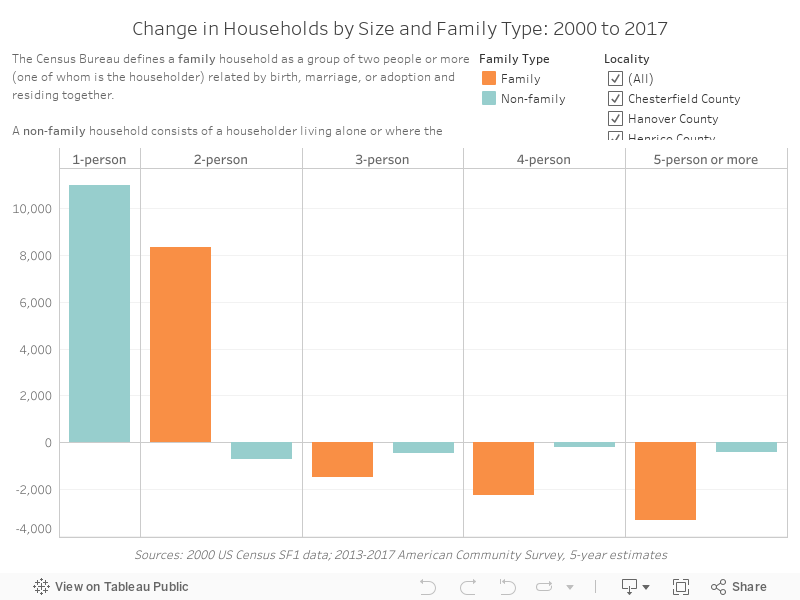

The Richmond Region’s Homeownership Market

Explore Homeownership Data

Where We’ve Been

Major public and private efforts to expand homeownership in the 1930s helped White households at the expense of Black households and neighborhoods of color.

In 1937, the Home Owners’ Lending Corporation (HOLC), a federal agency, graded Richmond neighborhoods from “A” through “D” to designate where government-backed home loans should be made. Communities with high concentrations of Black households, regardless of neighborhood quality or stability, were consistently rated “D”—the least desirable for investment. Marked red on maps, these “redlined” neighborhoods were systematically denied access to the same financing tools and wealth-building opportunities provided to White communities.

Why is redlining relevant today? One example: in 2016, the median household income in Richmond’s “A” neighborhoods was $95,800. In the redlined “D” neighborhoods, it was $32,800.

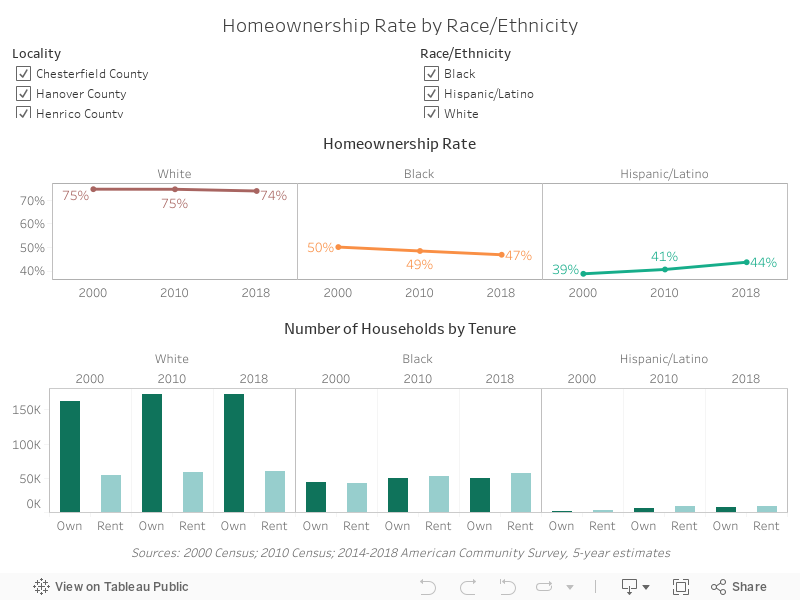

The Black homeownership rate in Virginia is lower today than it was 50 years ago, severely impacting the ability of Black households to grow, accumulate, and pass down wealth.

The Fair Housing Act of 1968 made discrimination in the housing market a federal crime. As of the 1970 Census, the homeownership rate for Black Virginians was 51.5%. Nearly half a century later in 2017, the Black homeownership rate in the state was 47.8%.

In the Richmond region today, three in four White households own their home, while fewer than two in four Black households do. While the total number of Black homeowners in Chesterfield, Hanover, and Henrico has steadily increased over the past two decades, there are nearly 4,000 fewer Black homeowners in the City of Richmond now than in 2000.

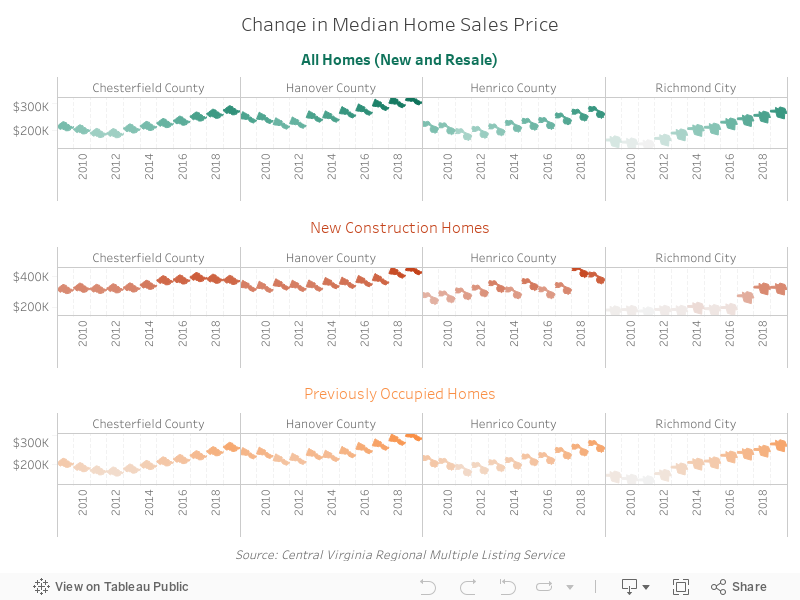

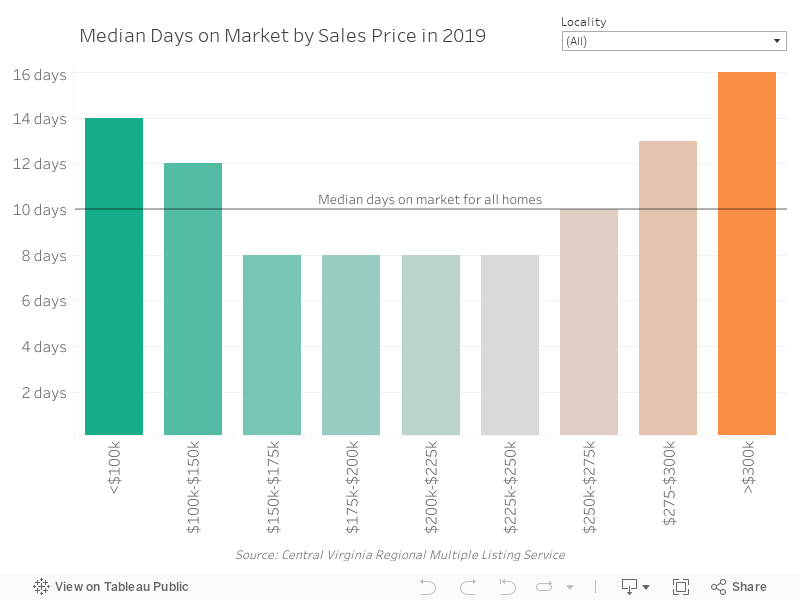

Home prices in the region have rebounded strongly since the recession.

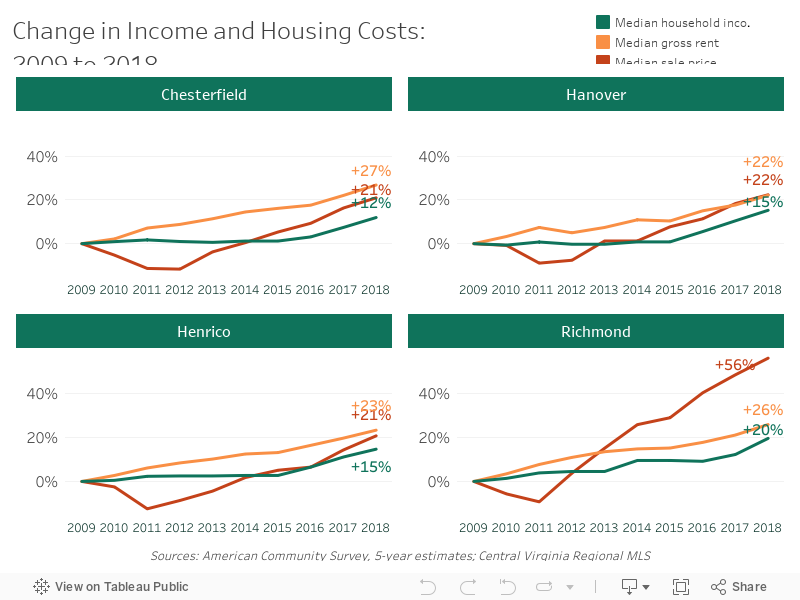

Over the past century, owning a home became one of the most successful ways for Americans to accumulate wealth and gain financial independence. Unfortunately, homeownership remains out of reach for many people throughout the region because our incomes aren’t keeping up with rising prices created by an extremely limited supply. Young professionals, working families, and seniors alike face major challenges looking for a home to buy in the Richmond region.

Furthermore, decades of discriminatory policies created—and continue to perpetuate—major barriers for Black and Latino people to purchase homes. This racial homeownership gap is a national problem, and the Richmond region is no exception. Today, our region’s homeownership rate for African Americans is a full 25 points lower than the white homeownership rate. Without intentional intervention to address housing patterns and the barriers to homeownership, the Richmond region will continue to be highly segregated and the racial wealth gap will remain.